IFRS 18 is no longer a proposal. The standard is set and it will change how organizations present and explain financial performance. While the mandatory effective date is January 1, 2027, the impact on reporting, governance and decision-making starts much earlier.

The revised income statement structure of aims to make performance clearer, more comparable and more transparent. That ambition is straightforward. Delivering on it requires organizations to make deliberate choices about how results are classified, how performance is explained and how those choices are embedded in processes and systems.

Organizations that act early avoid last-minute fixes and unnecessary complexity later. IFRS 18 is not just about meeting a new requirement. It is about taking control of how financial performance is communicated.

IFRS 18 forces clarity before compliance

IFRS 18 changes how financial performance is presented. Not by adding more rules, but by requiring organizations to clearly explain how their business works.

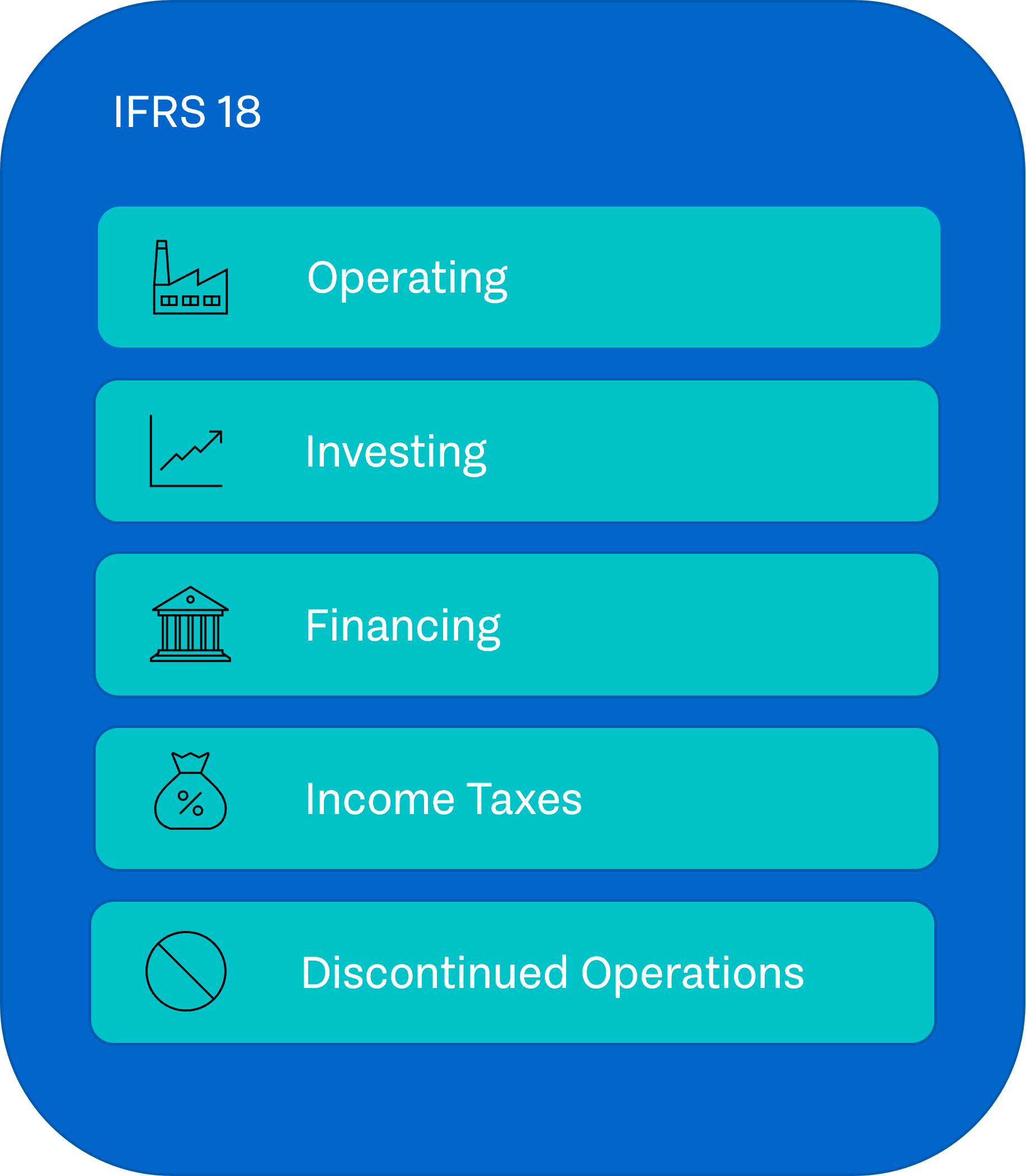

From 2027 onwards, income and expenses must be presented using five mandatory categories:

- Operating

- Investing

- Financing

- Income tax

- Discontinued operations

At first glance, this looks like a reporting format update. In reality, IFRS 18 challenges organizations to rethink how performance is structured, governed and explained. It touches your reporting model, your data, your systems and the way management talks about results.

That makes IFRS 18 less about accounting mechanics and more about design.

Why IFRS 18 cannot be solved with isolated fixes

Many finance teams instinctively start with the end product: the new P&L layout. That approach rarely works.

IFRS 18 introduces mandatory subtotals, stricter classification rules and formal requirements for management-defined performance measures. These elements are closely connected. A decision in one area immediately affects another.

For example:

- Presentation choices determine how results must be classified

- Classification depends on how accounts and data are structured

- Data structures determine whether reporting and MPM disclosures are reproducible and auditable

Treating these topics separately leads to workarounds, manual corrections and late-stage discussions with auditors. IFRS 18 requires a coherent approach, not a series of fixes.

That is why a clear, step-by-step setup matters, with clear roles between accounting judgment and reporting execution.

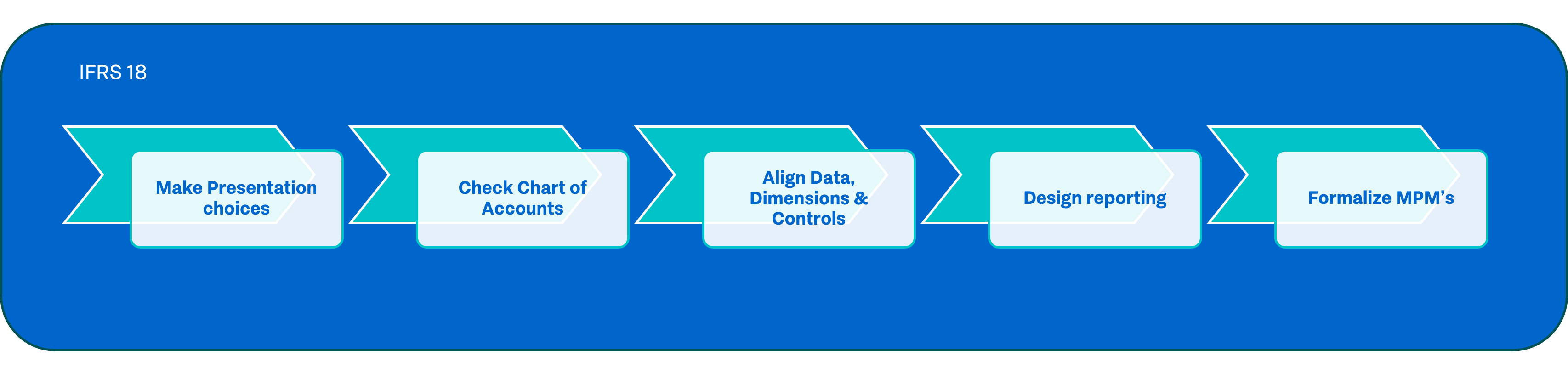

A structured way to approach IFRS 18

Organizations that stay in control approach IFRS 18 as a sequence of deliberate decisions. Each step builds on the previous one and removes ambiguity before it becomes a reporting issue.

Some of these steps are primarily driven by accounting interpretation. Others sit firmly in the domain of reporting, data and systems. Both are needed to make IFRS 18 work in practice.

Below is a practical way to structure that journey.

1. Make your presentation choices explicit

IFRS 18 reduces flexibility, but it does not remove judgment. It requires organizations to clearly define their logic.

Key questions include:

- What is Operating within your business model?

- What activities truly drive day-to-day performance?

- What belongs to Investing, such as associates, joint ventures or disposal results?

- What qualifies as Financing, including interest, derivatives and financing fees?

- How do you treat FX? Is it operational, financial or investment-related?

These choices directly determine mandatory subtotals like:

- Operating profit

- Profit before financing and income tax

Optional subtotals, such as Gross profit, are allowed, but only if they are consistent and well explained. These decisions are typically shaped together with your accountant, as they rely heavily on IFRS interpretation and audit alignment.

2. Check whether your chart of accounts can deliver

Once the presentation logic is clear, the next question follows naturally: can your chart of accounts actually support these choices?

Every P&L posting must map clearly to one IFRS 18 category. In practice, many organizations still use mixed buckets, such as:

- Combined finance income and expense

- Net FX results

- Other income and expense catch-all accounts

- Associates and joint ventures included in finance result

IFRS 18 exposes these structures. Deciding what should change, and what is acceptable from an IFRS perspective, is again closely linked to accounting judgment and audit requirements.

Clear separation is often also needed for:

- Interest on loans versus leases

- Financing fees versus interest expense

- Discount unwind or net interest on provisions

- Investment income

These distinctions are structural and will be scrutinized during audits.

3. Align data, dimensions and controls

Once the accounting logic is defined, the challenge shifts. The question is no longer what the rules are, but whether your data and systems can consistently apply them.

Typical questions at this stage are:

- Do we have dimensions or fields to support nature versus function reporting where relevant?

- Are recurring journal entries needed to reclassify items for IFRS 18 presentation?

- Can our consolidation system support two hierarchies during transition, the current view and the IFRS 18 view?

Controls become increasingly important. Validations such as “no unmapped accounts” or “no finance income in the operating bucket” help prevent inconsistencies before they reach external reporting.

This is where IFRS 18 becomes a data governance and reporting topic, rather than an accounting one.

4. Design reporting that is consistent and repeatable

With presentation logic, accounts and data aligned, reporting becomes the natural outcome rather than the starting point.

Organizations need to be able to produce:

- The new P&L with categories and mandatory subtotals

- Comparative figures

- Consistent labels and ordering

IFRS 18 also increases the visibility of certain items. Disaggregations that were previously less prominent may now attract attention simply because of where they appear in the statement.

Designing reporting that is repeatable, controllable and audit-ready is firmly part of the reporting and systems domain.

5. Formalise Management Performance Measures

Many organizations use adjusted measures such as Adjusted EBITDA or Underlying EBIT to explain performance. IFRS 18 does not remove these measures, but it does formalise them.

If adjusted measures are published externally, they are likely to qualify as Management Performance Measures (MPMs). This requires:

- A clear and stable definition

- A reconciliation to IFRS totals

- Consistent tagging of adjustments

While the definition is often agreed with accountants, the ability to produce these disclosures in a structured and automated way depends on how reporting and data are set up.

Manual spreadsheets quickly become a risk. Automating MPM disclosures from the ledger, with clear ownership and governance, creates both efficiency and confidence.

From regulation to control

IFRS 18 is not something you add on at the end of the reporting proces. It asks organizations to consciously design their reporting model, from accounting choices to data, systems and controls.

Accountants play a key role in defining the rules and interpretations. The real challenge, however, lies in making those choices work consistently in reporting.

At Finext, we focus on that reporting and data foundation. We help organizations translate IFRS 18 decisions into structures that are controllable, repeatable and future-proof.

IFRS 18 is not about doing more reporting.

It is about building reporting that makes sense.